FAQs - 2. Taxation-related matters

2-2) Please tell us more about consumption tax in Japan.

A) Overview of consumption tax

Japan’s consumption tax is a 5% tax on the sale price of items subject to this tax, such as retail goods, loans and services.

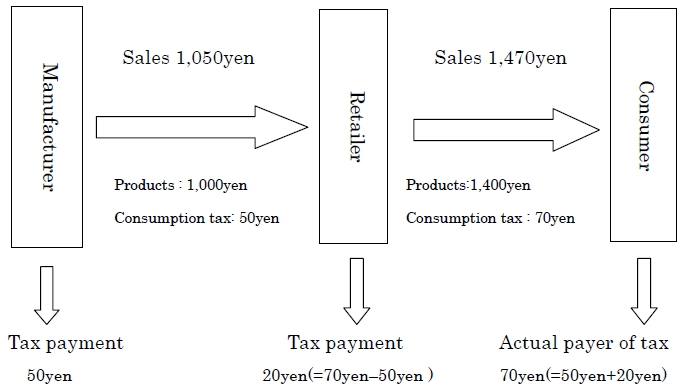

A business is obliged to pay an amount of tax representing the difference between consumption tax (from sales. Etc) it receives from others (from purchase etc) and consumption tax it has already paid (from purchasing activities etc)

B) Determining business subject to consumption tax

The obligation of a business to pay consumption tax or not is determined based on its amount of taxable sales(*2) within a base period(*1)

| Amount of taxable sales within base period | Subject to taxation |

| More than 10 million yen | Required to pay tax |

| Up to 10 million yen | Not required to pay tax |

In the case of a newly established company, since a base period does not exist for the 1st and 2nd year, this is determined by stated capital. If end-of-period capital is 10 million yen or more, the business is subject to consumption tax.

Also, when non-Japanese corporations establish a branch office in Japan, since a new company has not been established, this is determined using the head office’s amount of taxable sales within the base period.

(*1)What is “base period” ?

This is the business year two years prior to the current business year (also termed the period two years prior to the current period.)

(*2)What is “amount of taxable sales” ?

This is the monetary amount for transfer of assets (from sales etc.) conducted by businesses (corporate or individual) within Japan

C) Transactions not subject to consumption tax

The final consumer bears responsibility for payment of consumption tax on goods and services. Accordingly, some items are not considered subject to consumption tax and thus do not incur consumption tax. Also, certain kinds of transactions are not subject to consumption tax due to public policy considerations.

[ Non-taxable transactions ]- Transfer or lease of land

- Transfer of marketable securities

- Interest, insurance charges etc.

- Stamps, revenue stamps etc.

- Transfer of product vouchers etc

- Governmental or municipal administrative processing fees etc.

- Social insurance healthcare

- Transfer of books for educational purposes

- Transfer of books for educational purposes

- The social welfare industry etc.

D) Consumption tax for international transactions

Since transactions involving export from Japan are not Japanese domestic transactions, they are exempt from consumption tax. This follows international convention in that consumption of goods and services will be taxed directly in the country where they are ultimately consumed.

Export sales are exempt from consumption tax, and businesses can also receive exemptions on purchase tax for purchases involved in these sales.

On the other hand, imports to Japan are subject to taxation for the same reasons stated above.

E) Refund of consumption tax

For a business, the tax payment amount is calculated by deducting consumption tax already paid from total consumption tax received. For this reason, when the amount of tax that a business has paid exceeds the consumption tax it has received, it is eligible to receive a refund of this consumption tax payment. However, in order to receive this refund, it must be a "business subject to taxation"

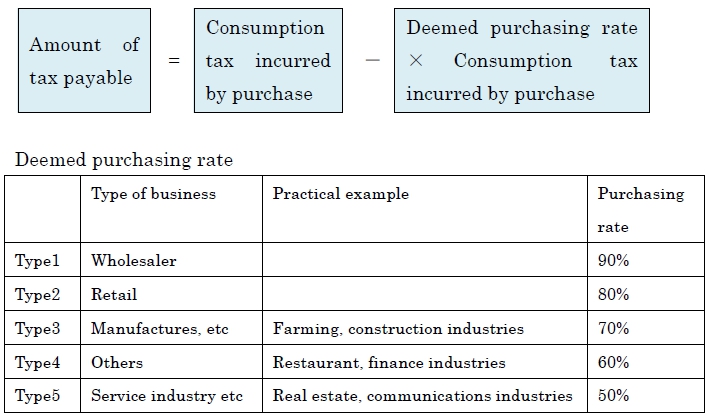

F) Simplified taxation system(special case)

The simplified taxation system is completely different to the methods explained previously. It is a method of estimating and calculating the amount of purchase tax by applying the specific purchasing rate designated for each category to the amount of taxable sales. However, when the amount of taxable sales in the base period exceeds 50 million, this method cannot be applied.

G) Businesses exempt from consumption tax may choose to become subject to consumption tax.

Those that do must submit a “Report on Selection of Taxable Proprietor Status for Consumption Tax” to their local Tax Office during the previous business year (or in the case that this is the first business year, during the current business year). When businesses exempt from consumption tax choose to become subject to consumption tax, for a 2-year period they may not return to being exempt from consumption tax (except in the case that the business is discontinued).

[ Note ]

Business exempt from consumption tax may pay excess consumption tax due to new construction of offices or purchase of machinery etc. in the previous period. By choosing to become subject to consumption tax, they may receive a refund of this consumption tax. It is necessary to provisionally calculate the company’s financial details in order to judge which option is more advantageous.