FAQs - 2. Taxation-related matters

2-10) Please tell us more about foreign income tax credits in Japan.

Since all income (both domestic and overseas) of Japanese corporations is subject to Japanese corporate taxation, the problem of international double taxation arises with regard to foreign income withheld at source.

In order to eliminate this international double taxation, in cases where Japanese corporations are paying foreign corporate tax, the following foreign tax credit system applies, under which these corporations are exempted from Japanese corporate tax and regional tax up to the amount of foreign corporate tax paid.

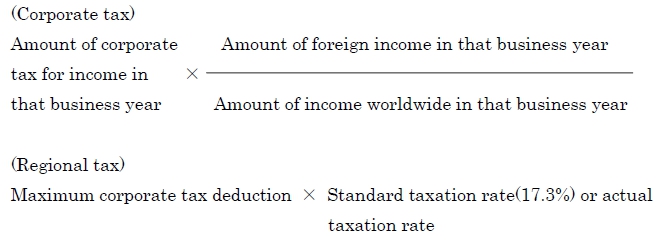

Note 1:The amount of foreign tax credit deductions is calculated as follows:

Note 2:Foreign tax credit deduction includes both direct foreign tax credit and indirect foreign tax credit.

Direct foreign tax credit is where the amount of directly paid foreign taxation (such as foreign corporate tax paid on profit from foreign branch offices or income tax paid on interest, dividends, royalties, etc, received from foreign companies) is not subject to Japanese corporate taxation.

Indirect foreign tax credit is where, in the case that dividends are paid by a foreign subsidiary to a Japanese corporation possessing 25% or more of the subsidiary company’s shares, of the amount of corporate tax paid on the income of that subsidiary company, the monetary amount of those dividends is recognized for the purposes of foreign tax credit.