FAQs - 2. Taxation-related matters

2-15) Please tell us more about salary payment in kind.

1. Definition of salary payment in kind

Although it is usual to receive monetary payment of salary or bonuses, it is also possible for these to be provided in the form of physical items, privileges, or other economic profits. This is termed salary payment in kind.

Some practical examples can be seen below.

(1) Provision of meals free of charge

(2) Provision of company housing at low rental cost

(3) Provision of monetary loans at low interest or no interest

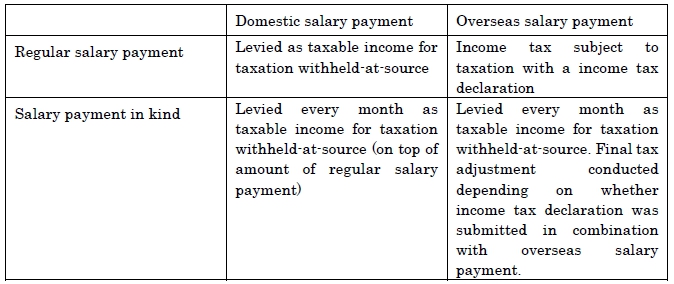

Company directors and employees, based on their positions, may be provided by the company with things other than their monetary salaries. After certain evaluations are conducted, these thing must be in their amount of salary income. When such provision is made, it must be added to the regular monetary salary for the purposes of calculating taxable income for taxation withheld-at-source.

Even those things that companies handle as fringe benefits costs may constitute taxable income for taxation with-at-source, and may be subject to taxation as salary payment in kind. Caution must thus be exercised.

2.Handling of payment in kind for employees dispatched from overseas corporations